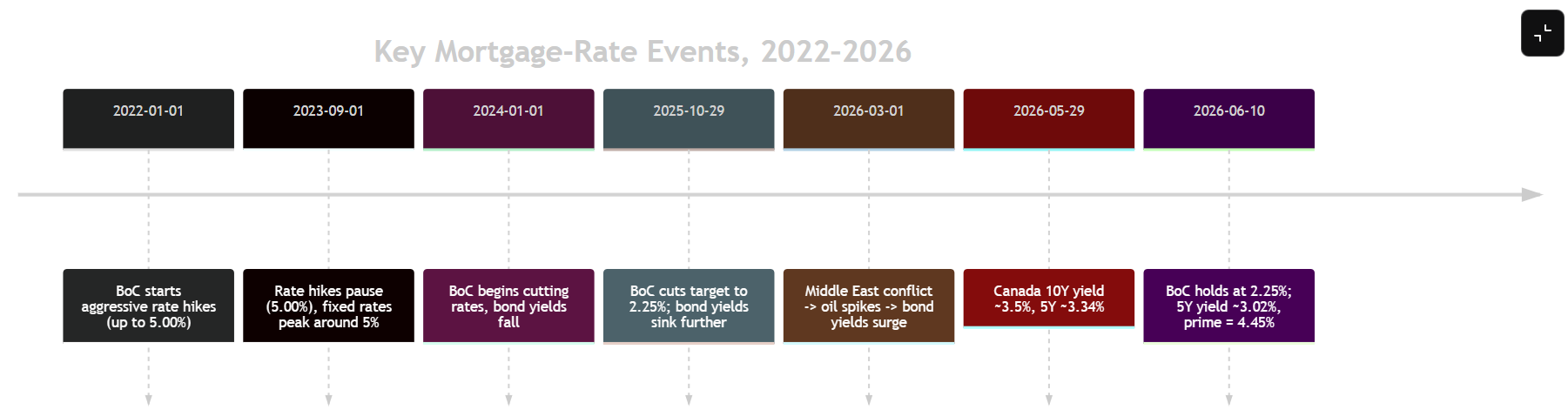

In mid-2026, Canadian borrowers face a critical decision; lock in a fixed mortgage or ride a variable rate? After years of Bank of Canada rate cuts, bond yields and fixed rates actually rose in spring 2026 (the five-year Canada yield hit ≈3.34% in May) before settling around 3.02% by mid-June. That pushed many posted fixed rates back into the low‑4% range. Variable (prime-linked) rates, by contrast, remain lower (prime ~4.45%). Economists expect the BoC to hold rates steady through 2026, so variable rates should stay around today’s level barring shocks.

Our detailed analysis, with charts, data tables and scenario modeling, shows that in a one‑year or two-year horizon, a variable mortgage typically costs less if rates stay flat or rise only slightly. As an example, assuming a $500,000 mortgage (25-year amortization), a 3-year variable at 3.65% would beat a 3-year fixed at 3.99% in total interest paid unless rates spike. (In our scenario runs, only a very large hike in 2027–28 erased the variable’s edge.) On the flipside, fixed-rate borrowers get certainty and can avoid any surprise hikes. Many homeowners now hedge by splitting or using a hybrid, combining fixed and variable to share the risk. We break down all these options also, comparing the costs under multiple “what if” scenarios, and offer a clear recommendation.

Key findings: Variable (prime) rates are currently ~3.65% for 3‑year terms (versus ~3.99% fixed) and around 3.3–3.4% for 5‑year (versus ~4.15% fixed). If rates only creep up a quarter‑point or stay flat, the variable option costs thousands less over a 3‑year term. But if inflation surprises and the Bank raises again in 2027–28, a fixed mortgage could be more cost‑effective.

Table of Contents

- Government Bond Yields in 2026

- Fixed-Rate Trends: 3‑Year vs 5‑Year

- Variable-Rate Outlook (as of June 2026)

- Fixed vs Variable: Cash Flow & Total Cost

- Scenario Analysis: Comparing 3% vs 4% Mortgages

- Pros & Cons of Fixed vs Variable

- Hybrid and Split Mortgage Strategies

- Conclusion & Next Steps

1. Government Bond Yields in 2026

Government bond yields underpin fixed mortgage rates. In 2026, Canada’s bond market saw a brief spike in spring due to global events. After the Bank of Canada held the policy rate at 2.25% into 2026, long-term yields had been drifting down until the Middle East conflict sent oil prices up, triggering a bond selloff. The 10‑year Canada yield jumped from about 3.12% in late February to ~3.47% by late May. Likewise, the 5‑year benchmark yield reached roughly 3.34% in mid-May before easing back to ~3.02% by mid-June.

Chart: Canada 5‑Year Government Bond Yield (Jan–June 2026) – After winter’s decline, yields spiked to ~3.34% in May (middle east war news) and then eased to ~3.02% by mid-June. Higher yields push fixed mortgage rates up. (Source: Bank of Canada / TradingEconomics)

In short, bond yields were back near two-year highs, though still well below their 2023 peaks. As Morningstar noted, “Canadian bond yields have pushed back to recent highs,” driven by oil-price inflation and rising U.S. yields. Given the Bank’s neutral stance, we expect yields (and fixed rates) to stay near these levels barring another shock.

This timeline shows the big picture: after cuts, inflation and geopolitical risk have pulled yields up again. Canada’s 5‑year bond yield, the usual benchmark for 5‑year fixed mortgages, sits around 3.0% as of today(June 17). As we’ll see, that translates into 5‑year fixed mortgage offers in the low‑4% area today. This is not as low as where we were at prior to the war in Iran, but still better than where they were at in mid-May.

2. Fixed-Rate Trends: 3‑Year vs 5‑Year

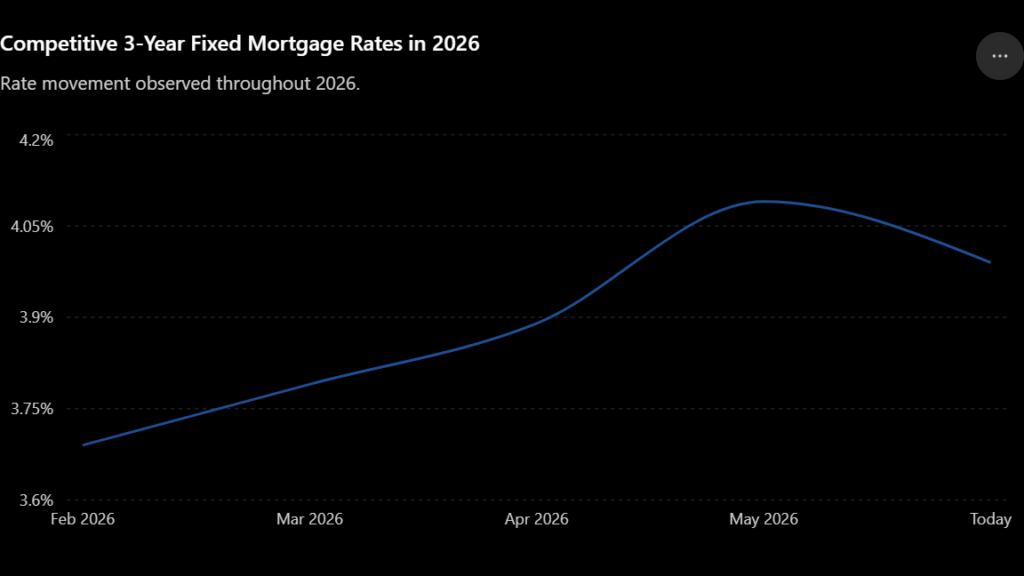

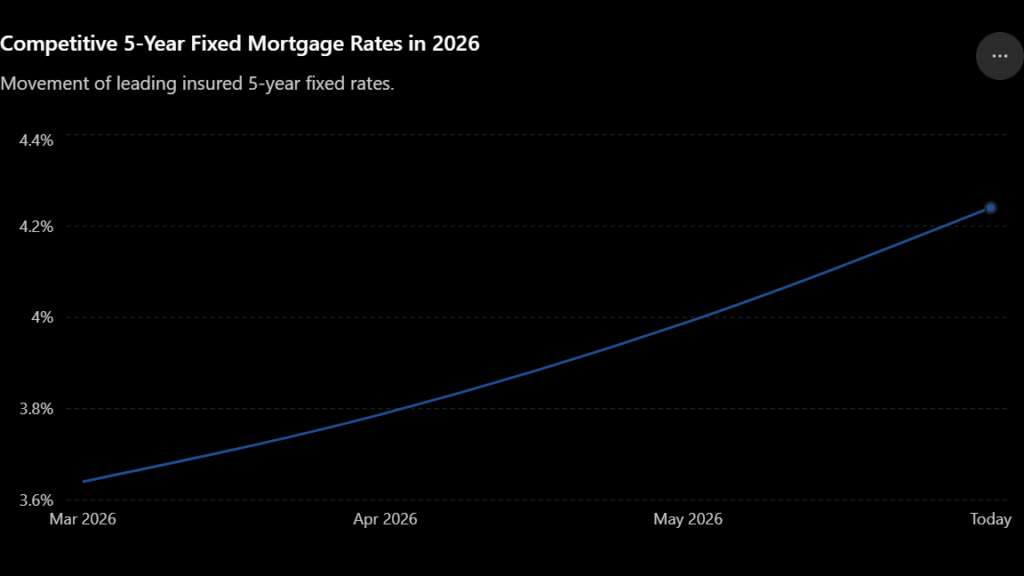

Canada has both 5‑year and shorter fixed-term mortgages. In 2022–2023, with BoC hiking aggressively, fixed rates rose above 5%. After cuts in 2024–25, by early 2026 fixed rates had eased. But the May 2026 yield spike pushed them back up. The charts below summarize recent trends:

Chart: 3‑Year Fixed Mortgage Rates (Jan–Jun 2026). Insured 3‑year fixed rates dropped to ~3.6% by late Feb 2026, then climbed into the low‑4% range by May before settling around 3.99% in mid-June. (Many borrowers see offers from 3.7–3.9% in spring.)

Chart: 5‑Year Fixed Mortgage Rates (Jan–Jun 2026). Insured 5‑year fixed rates were ~3.6% in spring 2026, then rose above 4.0% by May–June. (As of mid-June, the best 5‑year fixed offers are roughly 4.04% insured.)

In early 2026, some big banks were offering 3-year fixed rates as low as ~3.44% (insured). By contrast, 5‑year insured rates were around 3.64% in spring (see March row). Those rock-bottom offers disappeared in May; with the best rates now hovering in the 3.99% 3 year fixed/4.04% 5 year fixed range for insured mortgages.

To summarize: as of June 2026, fixed mortgages cost roughly 4.0–4.3% for 3‑ or 5‑year terms (depending on term and insurer, and whether the mortgage is insured). By comparison, prime-linked variable rates remain near 3.3–3.6% for similar terms (see next section).

3. Variable-Rate Outlook for 2026

Variable-rate mortgages in Canada are usually tied to the prime rate. With prime at 4.45% (given the 2.25% policy rate), most borrowers today see a 3‑year variable rate ≈ 3.65% and a 5‑year variable rate ≈ 3.3–3.4% (we use 3.65% and 3.45% in our tables below).

What will happen to variable rates? Because the BoC policy rate drives prime, it depends on the Bank’s moves. As of the June 10 announcement, the BoC held steady at 2.25% and gave no strong signal on future hikes. In fact, market odds of a 2026 hike are low: bond markets assign only ~6% chance of a July hike and ~18% by September. Many economists and polls now expect no change in the overnight rate for the rest of 2026. That implies prime (and variable rates) will likely remain around today’s levels unless something unexpected happens.

In summary, the variable-rate forecast is basically stable for 2026. If the Bank starts to cut later in 2027, variable rates would come down; if they hike slightly (e.g. to counter inflation), variable rates could rise. For now, however, our analysis assumes a starting variable rate of 3.65% on a 3‑year variable mortgage, stepping to 3.90% (scenario 2) or 4.15% (scenario 1) under modest BoC hikes next year (details below). These forecasts align with consensus: as one mortgage firm notes, “the BoC is likely to keep policy rates consistent for much of 2026,” so any drops in borrowing costs will be modest.

4. Fixed vs Variable: Cash Flow and Total Cost

Before choosing fixed or variable, it’s important to compare payments and total interest. We illustrate this with a $500,000 mortgage, 25-year amortization – roughly the Canadian average. Below is a 3-year comparison:

- 3-Year Fixed at 3.99%: Monthly payment = $2,636. After 36 months, total interest paid ≈ $57,731, and principal outstanding ≈ $462,820.

- 3-Year Variable at 3.65% (initial): Monthly payment = $2,543 (assuming full 25-year amortization). If rates remain at 3.65% for the full term, interest and payments would stay lower than fixed.

However, if the BoC raises rates, the bank will typically recalculate the variable mortgage payment at each rate change (to amortize in the remaining term). For example:

- If the rate rose by 0.25% in 2027 (to 3.90%), the new payment (starting year 2) would rise to $2,609.

- If the rate instead rose by 0.50% (to 4.15%), the year-2 payment would be $2,676.

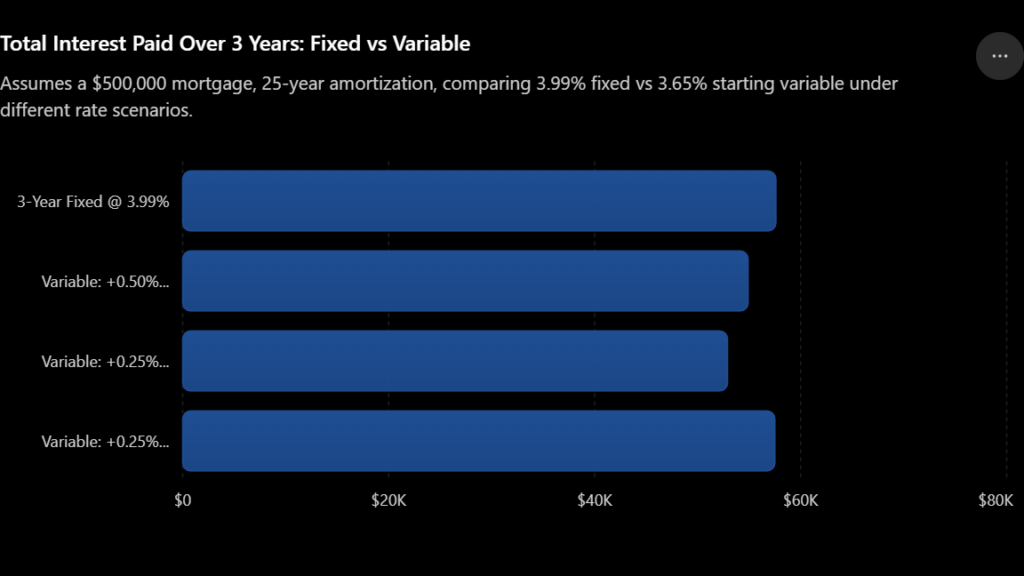

The table below compares total interest and remaining balance under each scenario. In all cases we compare a fixed 3.99% mortgage versus a 3.65% variable that bumps up (1) 0.50% once, (2) 0.25% once, or (3) 0.25% then another 0.50%. (See Appendix for calculation details.)

| Scenario | Year 1 Rate | Year 2 Rate | Year 3 Rate | Total Interest (3 yrs) | Ending Balance |

|---|---|---|---|---|---|

| 3.99% fixed (benchmark) | 3.99% | 3.99% | 3.99% | $57,731 | $462,820 |

| Variable, +0.50% in 2027 | 3.65% | 4.15% | 4.15% | $57,537 | $462,787 |

| Variable, +0.25% in 2027 | 3.65% | 3.90% | 3.90% | $55,128 | $461,980 |

| Variable, +0.25% (2027) +0.50% (2028) | 3.65% | 3.90% | 4.40% | $57,489 | $462,784 |

(All calculations assume $500k loan, 25-year amortization. Fixed/variable payments are recalculated to amortize the remaining balance after each rate change.)

From this table we see:

- Scenario 2 (small hike): The variable mortgage clearly wins. Even with a 0.25% rise, total interest ($55,128) is $2,603 less than the fixed-case ($57,731), and payments are lower in each year.

- Scenario 1 (moderate hike): The variable mortgage is still slightly cheaper overall ($57,537 vs $57,731), saving about $194 in interest. Payments bump up, but overall cost remains comparable to fixed.

- Scenario 3 (two hikes): A more severe path (0.25 + 0.50) nearly erases the advantage: total interest $57,489 is still a hair below fixed, but only by ~$242. Essentially it costs about the same as fixed in this worst-case.

Chart: Total Interest Paid (3-Year Term) – A bar chart comparing total interest under a 3.99% fixed vs three variable-rate scenarios (starting 3.65%). Unless there are substantial future hikes, the variable option costs less over 3 years. If the Bank hikes aggressively (Scenario 3), the costs converge (all around ~$57.5K–$57.7K).

Key takeaway: If future rates are flat or rise only modestly, a variable mortgage costs thousands less than locking into 3.99%. Even with a +0.50% hike, the total interest is nearly the same (within a few hundred dollars). Only in the scenario of multiple hikes (+0.75% total over 2 years) does the fixed rate begin to “win.” In practice, of course, borrowers can prepay or refinance on a variable if rates rise, which adds flexibility (see below).

Of course, borrowers often ask about monthly payments rather than total interest. The fixed-rate mortgage here had a higher payment ($2,636) than the initial variable payment ($2,543), which matters for cash flow. But variable payments do rise when rates go up. In Scenario 1, the year‑2 payment was $2,676 (still comparable to fixed). In Scenario 3, the third-year payment hit $2,739. Each borrower must weigh: can my budget absorb a higher payment if rates change? Keep in mind that some lenders offering variable rates will not change your monthly payment; they will simply recalculate how much of that payment goes to principal vs interest if the prime rate changes.

In summary, on cost alone the variable mortgage is generally cheaper or equal under most expected cases. The remainder of this article digs into the qualitative tradeoffs and advanced strategies.

5. Pros & Cons of Fixed vs Variable

Fixed-Rate (Pros):

- Payment Certainty. Your interest rate and monthly payment are locked for the term (e.g. 3 or 5 years), making budgeting easy.

- Protection against Hikes. If the Bank raises rates or bond yields jump, you’re sheltered. This peace-of-mind can be worth a premium for many.

- Longer Term Options. 5-year fixed terms are available (and favored by most buyers); by contrast, variable mortgages usually have 3- or 5-year amortization schedules tied to prime.

Fixed-Rate (Cons):

- Higher Rate/Premium. Fixed rates include a spread over bond yields. In our analysis, a 3-year fixed was ~0.34% higher than comparable variable (3.99% vs 3.65%). Over 25 years, that extra margin adds thousands in interest (unless rates rise dramatically).

- Lower Prepayment Privileges. Many fixed deals come with stricter penalties.

- Opportunity Cost. If rates fall, you’re stuck paying a high fixed rate until renewal (though we think rates have likely bottomed out for now).

Variable-Rate (Pros):

- Lower Starting Rate. Currently, prime-based rates are 3.3–3.7% for 3–5 year terms, well below posted fixed rates. That yields big savings if rates don’t climb much. Our scenarios showed a variable could save ~$2,500 in interest over 3 years with only a 0.25% hike, versus fixed.

- Prepayment Flexibility. You can break/transfer a variable mortgage with a small three-month interest penalty (versus higher fixed penalties).

- Rate Convergence. You can lock in a variable rate as a fixed rate later should you want to. This involves no fees or penalties to do so.

Variable-Rate (Cons):

- Uncertain Payments. If inflation or BoC policy surprises, your rate (and often your payment) can rise. You must be comfortable with the potential volatility.

- Budgeting Risk. If your cash flow is tight, even a modest hike could be painful. Some borrowers would rather pay a slightly higher rate for budgeting certainty.

- End-of-Term Risk. At renewal, if fixed rates have fallen, you won’t capture that with a variable. (Though you could refinance again.)

Can you switch mid-term? Yes. One advantage of a variable mortgage is that many lenders let you convert it to a fixed rate during the term, usually by paying the difference between rates. For example, if you signed a 5-year variable and after 2 years decide rates are too risky, you could lock into a 3-year fixed at the then-current market rate (or vice versa). This flexibility is often cited as a safety valve: start variable, then fix later if you feel rates have bottomed.

Debt Splitting or Hybrid Mortgages: Many borrowers use a blend strategy: splitting their mortgage into two parts. For example, you might take 50% on a 5‑year fixed and 50% on a 3‑year variable. This hedges your bets. The fixed half protects against big hikes, while the variable half keeps initial costs down. If markets are uncertain, this mix can offer both stability and upside. (For instance, if rates unexpectedly fall, your variable portion benefits.) There’s no rule here, as some even do 70/30 splits. The key is aligning the split with your risk comfort. Talk to your broker about “split mortgages” or “combination mortgages” to see if it makes sense for you.

6. Hybrid and Split Mortgage Strategies

As noted, hybrids (splitting your mortgage between fixed and variable, or across terms) are popular. Here are some practical examples and tips:

- 50/50 Split (Fixed/Variable): If you have a $500k mortgage, you could fix $250k at 5‑year and put $250k on a 5‑year variable. Your blended rate equals the average. Even if variable rises, only half your balance is affected. On the flip side, if fixed rates trend down, your fixed chunk won’t benefit – but you still capture some savings via the variable half.

- Different Terms: Suppose you fear jumps but still want some flexibility. You might take $300k at 5‑year fixed, and $200k at 3‑year variable. When the 3‑year variable expires in 2029, you could roll it into another fixed if conditions make sense.

- Offset Mortgages: Some fixed mortgages allow an offset account (savings account that offsets interest). This doesn’t exist with variable mortgages. If you have short-term cash cushions, the offset can effectively lower your interest paid.

These options can get technical, but a mortgage broker or lender can tailor them. The goal is to hedge your unique risk tolerance. Nothing prevents you from converting your approach at renewal: if you start variable and after 18 months of rising rates decide to fix, you can likely do so with a new 3‑year fixed contract.

7. Conclusion & Next Steps

So, which wins? The data show that in most likely scenarios, starting variable makes more sense in June‑2026. Unless you very strongly want stability or absolutely cannot risk any rate rise, the variable-rate option could save you money over a typical 3‑ to 5‑year term. (In contrast, if the BoC were near cutting next, fixed would gain appeal, but currently cuts are off the table.)

However, the best mortgage is not just about the lowest number. Before renewing or refinancing, ask yourself:

- Do I have wiggle room in my budget for a higher payment if needed?

- Am I comfortable watching my rate float, or do I prefer set-it-and-forget-it?

- Might I move or refinance in the next 1–2 years anyway?

- What prepayment or portability features do I need?

Finally, don’t accept your lender’s first renewal offer without checking alternatives. Even with the war and yields, there are competitive fixed and variable promos out there.

Each of these steps could save you hundreds or thousands over your next term. In the current environment, even a small rate change matters so make the most of it!