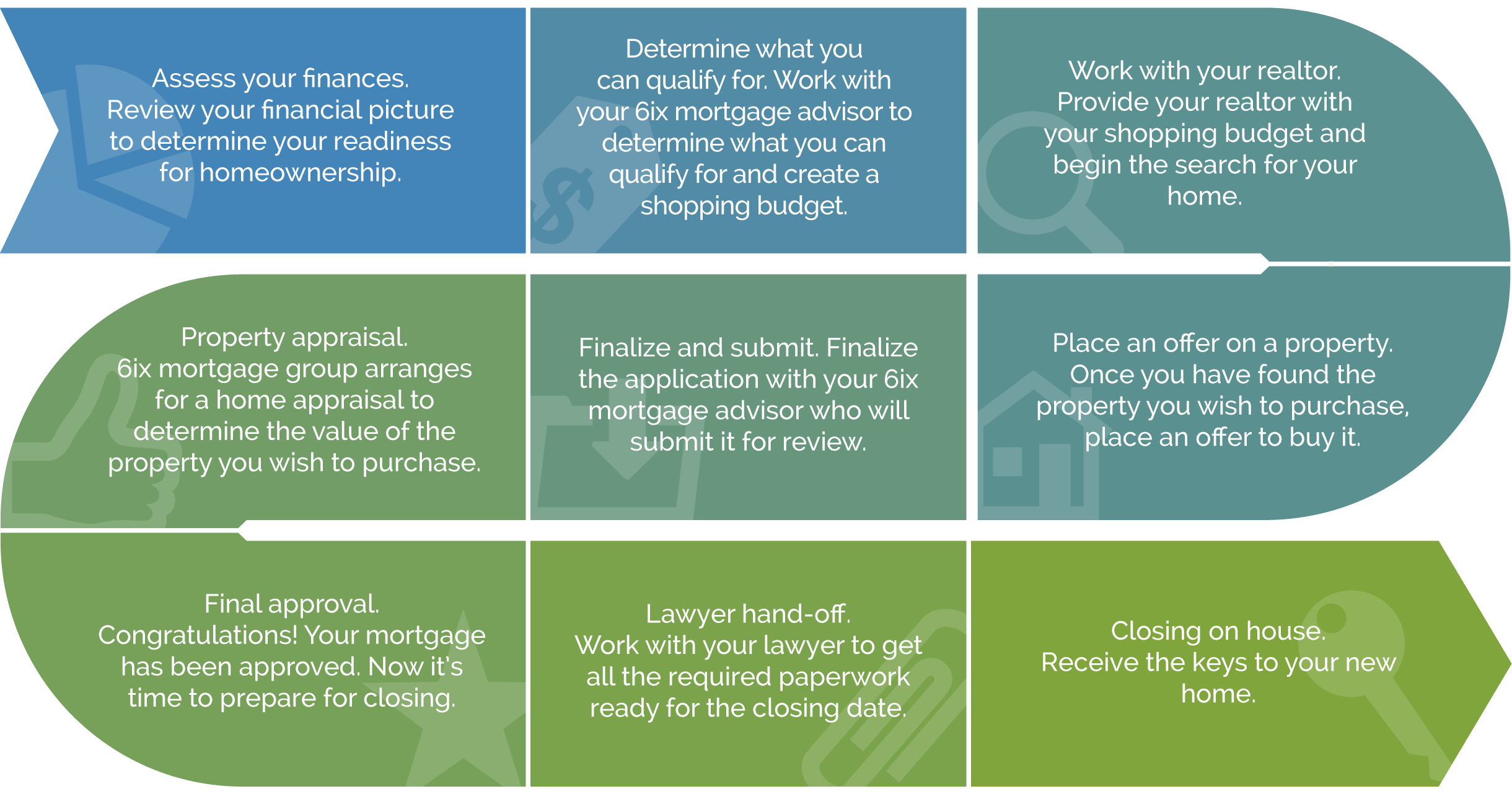

If you own a home, using the equity you have built up may be one of the most cost-effective ways to lower your borrowing costs. In many cases, home equity lines of credit can offer you a lower interest rate as compared to other types of loans while providing you with access to credit for unexpected expenses or home improvement projects. It’s yours to use however you wish!

You may be able to borrow against the equity in your home to finance other needs such as a home renovation, debt consolidation, college tuition and more. You can generally borrow up to 80% of the appraised value of your house.

Advantages of a Home Equity Line of Credit

1. You can access up to 80% of your home’s value

In Canada, you can access up to 80% of the value of your home through a home equity line of credit. However, it’s also important to remember that your outstanding mortgage loan balance + your HELOC cannot equal more than 80% of the value of your home

2. Your HELOC funds will be available through a revolving line of credit

With a home equity line of credit, the entire credit available is not advanced upfront. Instead, you can use as much or as little of the HELOC as you choose, and you only pay interest on the amount you withdraw. You can reborrow whatever you pay back.

3. You make interest-only payments

If you are using any portion of your home equity line of credit, you will need to make a monthly payment. Your contractual payment is interest only; however, you can pay as much as your budget allows without any penalties.

Get Started

An Equity line of credit is good to have in the event something unexpected comes up. Talk to one of our experts to determine what type of Equity Line of credit is right for you.

If you own a home, using the equity you have built up may be one of the most cost-effective ways to lower your borrowing costs. In many cases, home equity lines of credit can offer you a lower interest rate as compared to other types of loans while providing you with access to credit for unexpected expenses or home improvement projects. It’s yours to use however you wish!

If you own a home, using the equity you have built up may be one of the most cost-effective ways to lower your borrowing costs. In many cases, home equity lines of credit can offer you a lower interest rate as compared to other types of loans while providing you with access to credit for unexpected expenses or home improvement projects. It’s yours to use however you wish!