The Bank of Canada announced today that it’s holding its overnight rate at 2.25%, marking the sixth straight rate announcement with no changes.

At this point, it shouldn’t come as much of a surprise! It seems that the Canadian economy is still moving, but with some caveats. Inflation has come down significantly from its peak, but it’s still high enough that the Bank of Canada isn’t ready to start cutting rates or raising them.. For now, we are in a holding pattern.

Why Is the Bank Holding Rates?

On one hand:

- Economic growth has been relatively slow.

- Unemployment has ticked higher than we’d like.

- The housing market, especially here in Ontario, remains much quieter than it was a few years ago.

On the other hand:

- Inflation hasn’t completely settled.

- Global uncertainty (trade tensions, oil prices, geopolitical events) continues to create risks.

The Bank of Canada doesn’t want to stimulate the economy too much while inflation is still above where they’d like it to be.

Homeowners Are Still Feeling the Pressure

Even though rates haven’t increased recently, many Canadians are still dealing with the effects of the rate hikes from the past few years.

A lot of homeowners who were paying around 2% on their mortgage are now renewing closer to the 4% mark.

That’s money that isn’t going toward vacations, renovations, investments, or paying down other debt, its going straight towards interest on your mortgage.

This is one of the reasons the economy looks “okay” on paper, but many families still feel financially stretched. We have found that many borrowers are re-amortizing their mortgages on renewal to free up cash flow, or at least not take as large of a bump up in monthly payments from the lower rates they are coming out of.

Variable Rates Are Becoming More Popular Again

This has probably been the biggest change we’ve noticed this year.

For the last few years, fixed-rate mortgages have been the main choice for borrowers because variable rates became significantly more expensive, or the spread difference did not warrant going variable for the risks associated with it(we all remember post 2021!).

Now the opposite is happening. Today we see some of the best variable rates around 3.40%, while the best fixed rates are sitting around 3.84%.

That’s more than a 0.40% spread, which is causing many borrowers to take another look at variable rate mortgages.

On our own mortgage book, we’ve seen variable mortgages increase by roughly 15% since 2024.

Fixed rates are still the most popular option overall, but variable is making a strong comeback.

Why Fixed Rates Keep Moving Around

A lot of people assume the Bank of Canada controls all mortgage rates, but that is not true. The Bank of Canada directly influences variable-rate mortgages through the prime rate. Fixed rates, however, are mainly driven by Canadian bond yields, which change daily.

That’s why you’ve probably noticed fixed rates changing even when the Bank of Canada hasn’t moved.

Bond markets react to things like:

- Inflation expectations

- Government spending

- Oil prices

- Global conflicts

- Economic data

Over the past few weeks we saw fixed rates begin to fall as bond yields declined. Recently, rising oil prices and renewed global uncertainty have pushed bond yields back up, reducing the chances of lenders making further fixed-rate cuts in the short term. This means that in the short term outlook, fixed rates could start going up again.

My personal opinion is that if you snagged a fixed rate below 4% in 2026, you did good.

What Happens Next?

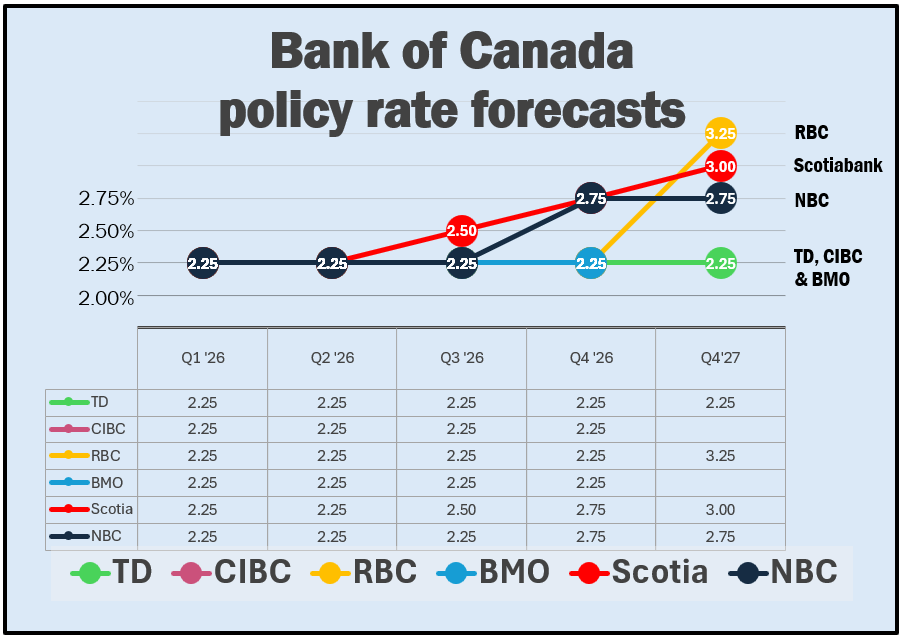

Most of Canada’s Big Six banks now expect the Bank of Canada to leave rates exactly where they are throughout 2026.

Where opinions start to differ is 2027. Some banks believe the next move will actually be higher, with forecasts ranging from 2.75% to 3.25% by the end of 2027.

Keep in mind that these are just the current forecasts. Economic forecasts change constantly, and it only takes one major inflation surprise or global event to shift expectations.

My Take

If you’re renewing your mortgage this year, I wouldn’t base your decision solely on where you think rates are going.

Instead, think about the following:

- Would you lose sleep if variable rates increased?

- Would you rather have payment certainty for the next few years?

- Or are you comfortable with some fluctuation in exchange for a lower starting rate?

The good news is that borrowers finally have meaningful choices again. Variable rates are competitive, fixed rates have come down considerably from their highs, and both options have their own pros and cons. Variable rates can be converted into a fixed rate at any time(with no fees or penalties), and carry a much smaller penalty to break if you are thinking about ending your term early. Fixed rates provide predictability in budgeting and payments, and often have better port options than variable rates.