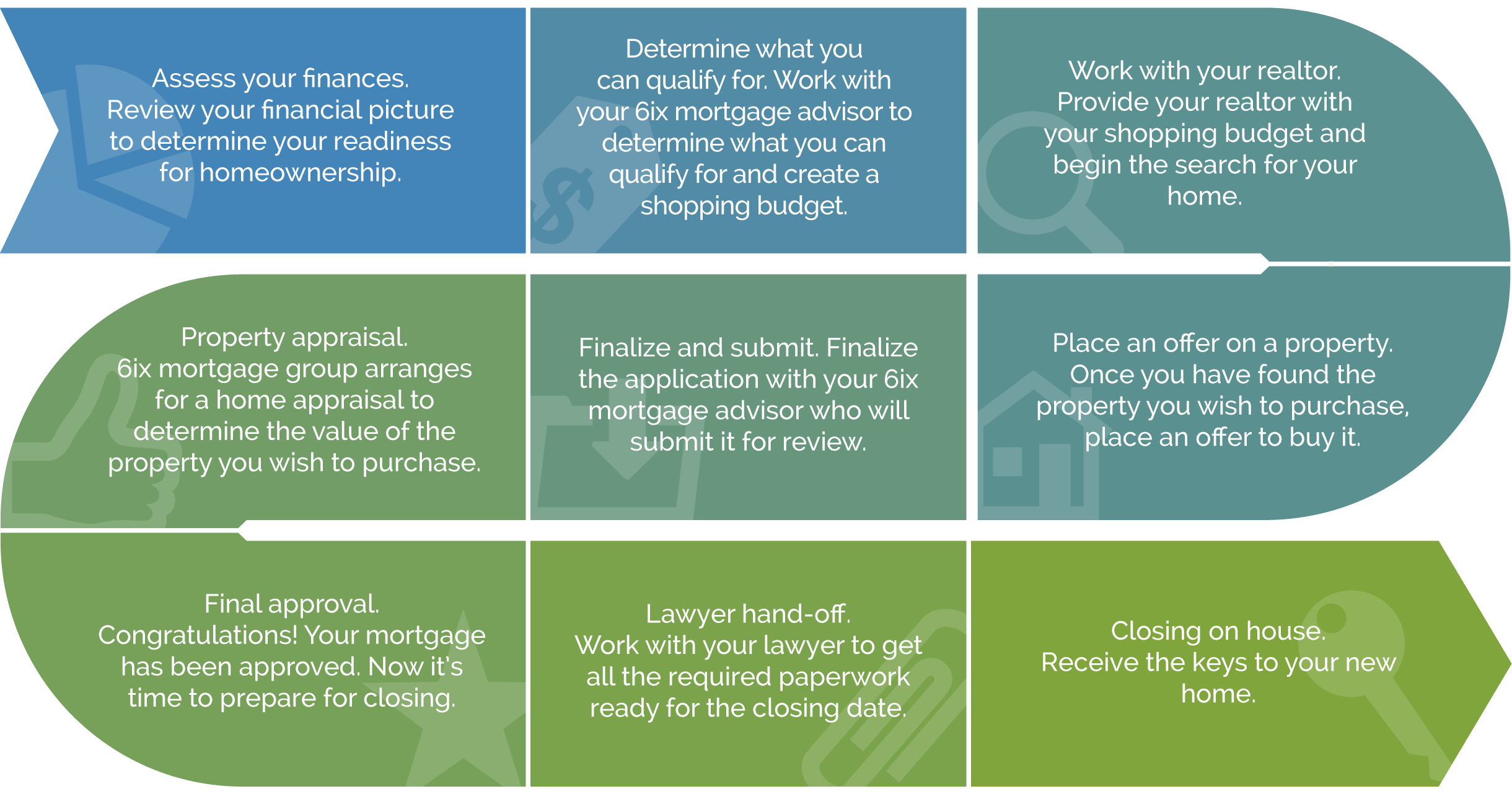

Real estate is of the best strategies many investors use for building wealth. However, you need to be aware of what’s involved in this complex art of investing? Our experts at the Mortgage Architects will guide you through a step by step process in the journey of achieving financial freedom through landing your first investment property mortgage.

Purchasing an investment property is very different than purchasing a property you would be residing in. Are you looking to bank on capital appreciation or are you looking to be cash flow positive? We look at your entire financial portfolio to determine what makes sense.

There is more than one way to finance an investment property in Ontario. At the Mortgage Architects, we create a customizes plan based on how long you plan to own the property, your cash flow needs and the amount of capital you are prepared to inject.

What is Investment Property Mortgage in Ontario?

An investment property mortgage is a form of loan provided to real estate investors who want to acquire rental properties. Qualifying for an investment property mortgage is often more difficult since you are required to prove you will receive significant income from the property. Additionally, prove if you are able to afford to uphold it with your liquid assets even in times when it is not generating profit, such as during the first six months of acquiring the property or during renovation.

Main differences between residential and investment property mortgages:

Higher down payment

Investment property mortgages in Ontario require a significantly greater level of financial stability than residential houses, especially if the property will be rented out. For investment homes in Ontario, most mortgage lenders need at least a 15-20% down payment, which is normally not necessary when purchasing your first house.

Higher credit score requirement

A higher minimum credit score is often required to qualify for a loan to buy an investment property in Ontario. You may get conventional financing for the main house with a credit score as low as 620. The minimum credit score for an investment property ranges from 640 to 680, depending on whether you acquire a fixed-rate or adjustable-rate mortgage.

Possibly higher interest rate

Another difference is that you’ll pay a higher interest rate when financing an investment property in Ontario. This is due to the fact that lenders view investment homes as a higher risk than a primary house.

All of these may sound discouraging for potential individual or partner investors, but it doesn’t stand in the way of establishing a successful investment property. As long as the processes are in the right hands, your gains will nonetheless outweigh the costs in the long run. Rental revenue will not only help you make money, but it will also help you pay off the loan you took out to buy the home in Ontario and even help you qualify for even better loan terms.

Other Considerations

Want to give yourself an edge over others applying for investment property mortgages in Ontario? Then keep these in mind:

Regular homes are not investment properties

Many people make the mistake of thinking their current home is investment enough. However, investment properties function differently from residential properties since you will be renting or leasing out the property.

Get preapproved for a mortgage in Ontario

remember that a prequalification is not the same as a preapproval for a mortgage. Getting preapproved not only provides you with a detailed guide of how much money you can allocate during property shopping, but it gives you an edge during property bidding.

House flipping cost-benefit analysis

If you’re considering taking out an investment property mortgage in Ontario for a low-valued property and then flipping it for revenue, make sure to evaluate all of the costs and benefits associated with it. This includes but is not limited to how much renovations will cost in relation to the estimated revenue and property value.

Look around for the best lender

Finding an optimal lender for investment properties in Ontario is difficult, especially without many federal options available. Find a private lender that provides you with the best deal and rates. This is especially cost-efficient if you are able to negotiate for a higher down payment in exchange for a lower interest rate.

Be mindful of your liquid assets

Generally, you will be required to show evidence of savings or liquid assets that can be easily converted to cash to qualify for an investment property mortgage. Ensure that this amount covers at least six months of expenditure needs for maintaining the property before applying for your mortgage.

Here are some of the more common mortgage solutions for investment properties in Ontario:

Assigning a conventional mortgage to your investment property is common. Based on your down payment, the income from the investment property should cover the Principal and Interest payments and provide a contingency fund.

Establishing a home equity line of credit on your principle home to pay for the investment property in Ontario is also a viable option for some. This is a also a safe strategy if you are investment for a short term.

Mortgage Architects offers a unique product for seasoned investors. Your contractual payments are interest only, therefore you end up cash flow positive on your property. This is also a good option for short term flips.

The amount of your down payment is a critical factor in establishing a long-term and reliable return on your investment. Work with your Realtor and your Mortgage Architects expert to determine the most cost-effective down payment amount based on the value of the property and its income potential. More might not always be better.