Buying from a Builder (Pre-Construction Financing)

Choosing to buy a new home from a builder can be a great option when you want to customize your home, but don’t want the responsibility and pressure of acting as your own general contractor. While buying from a builder may not be as involved as building your own home, it still requires some sound financial planning.

At the Mortgage Architects we will guide you every step of the way, so that you know what to expect when it comes to financing your new home.

Our Experts can provide you with:

- Firm, fast approvals

- Direct communication with your builder to streamline the financing process

- Straightforward advice on the financing options available to you

- An interest rate guarantee which locks in a competitive rate while your home is being built

- Financing solutions for Builder upgrades

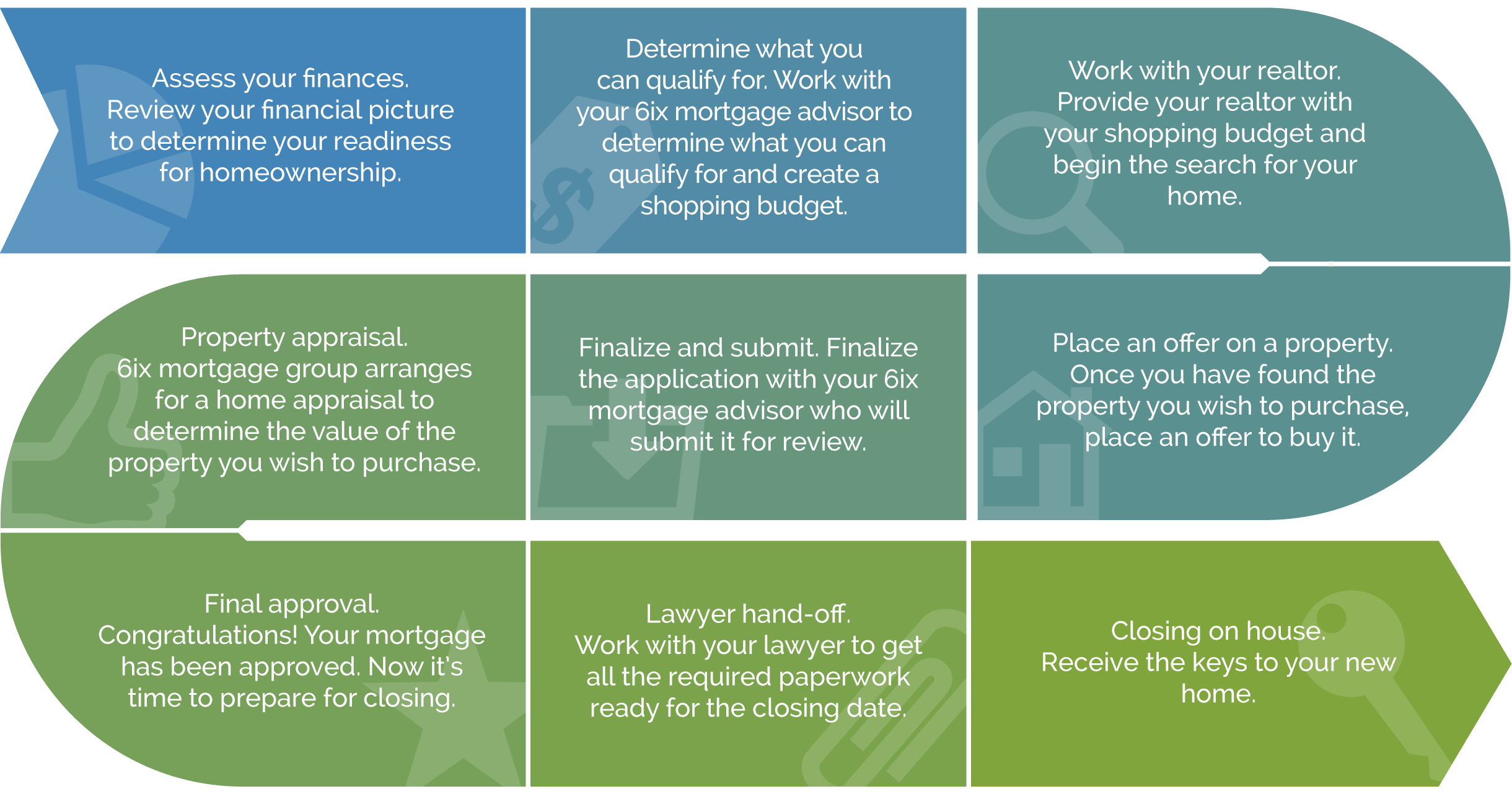

THE HOME BUYING PROCESS

Required Mortgage Documents Checklist

- Current employment and amount of income such as:

- Copy of recent pay slips

- Evidence of recent pay deposited electronically

- T1 General and associated Notice of Assessment (NOA)

- Previous employment (if required)

- Additional income sources (if any)

- Savings or investments statement from within the last 90 days

- Sale of an existing property – a copy of the sale agreement

- Withdrawal from RRSP through the Home Buyer’s Plan, if applicable

- Gift Letter

- A list of current assets and liabilities

- Bank account and transit number for payments

- Your CIBC Pre-Approved Mortgage Certificate, if applicable

- A copy of the real estate listing

- A copy of the accepted purchase and sale agreement

- The property’s full address, including legal description and postal code

- Property tax estimates, condo fees and heating costs, (usually available on the real estate listing)

- For rural properties, well and septic certificates

- Lawyer’s name, address, postal code, telephone and fax number