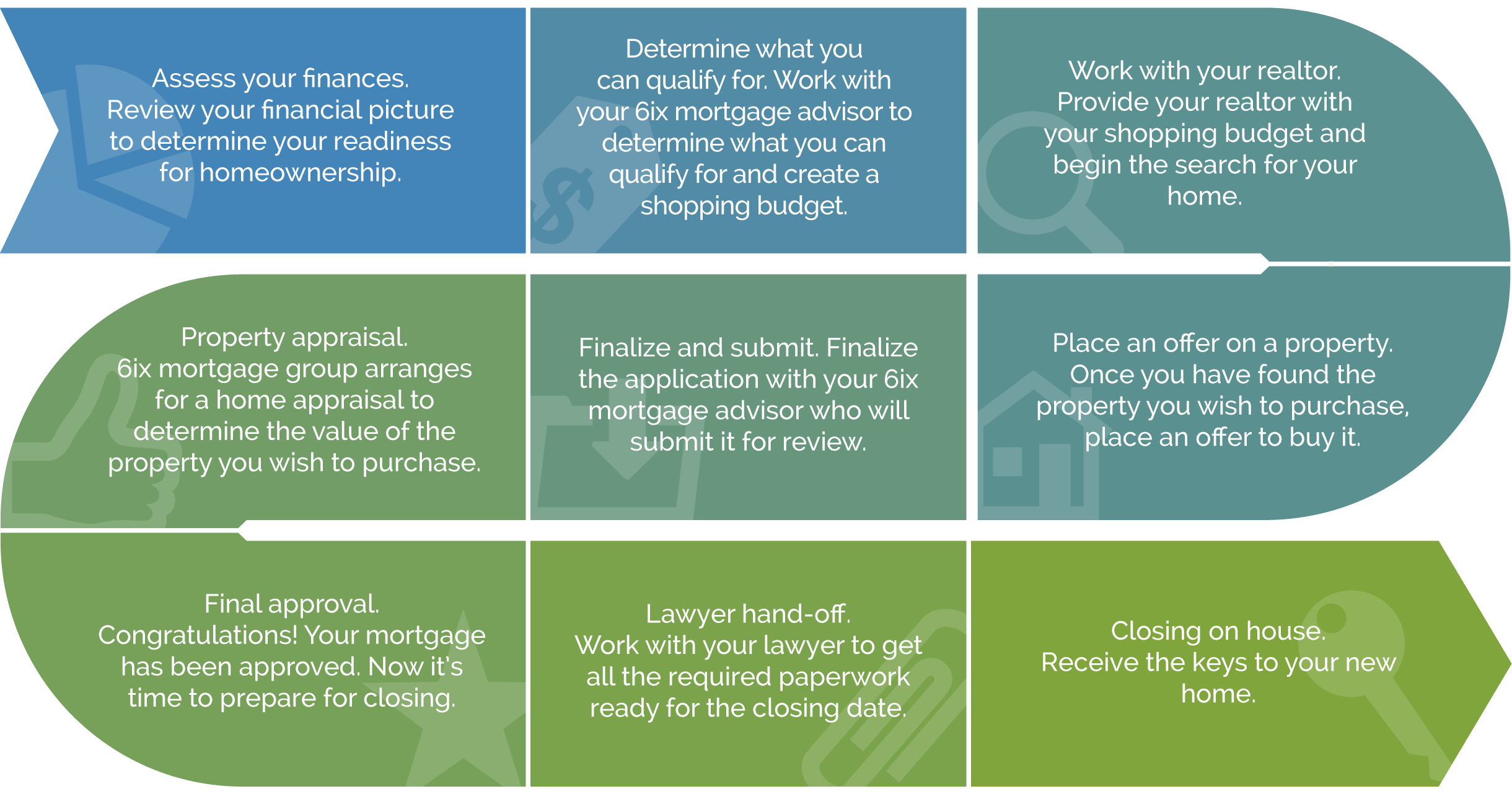

At the Mortgage Architects, we will be with you every step of the way. We’ll make sure that you understand your options, the first time home-buying process and when to engage the other professionals who make up your home-buying team.

What You need to consider?

Affordability

At the Mortgage Architects we start with preparing a customized financial blueprint for you during your first time home buyer journey. This highly customized plan covers your budgeting, lifestyle and property needs. Our goal is to ensure your mortgage payments will not add undue stress to your budget.

Closing costs

There are costs associated with closing a home. From legal fees to land transfer tax. We ensure you are fully prepared for every type of expense you may encounter.

Fixed versus variable interest rate

Mortgage payments reduce the interest owing on your loan while they reduce the principal amount that you owe. In the first term of your first mortgage, most of your payment will be allocated to interest charges. By your final term, the opposite will happen.

With a fixed-rate mortgage, your interest rate will not change throughout the term of your mortgage.

With a variable rate** mortgage, your payment amount stays fixed for the term; however, the interest rate will fluctuate with any changes in our prime interest rate.

Get pre-approved and shop with an advantage

A no-cost, no-obligation pre-approval gives you several advantages in today’s competitive housing market.

When you get a first time home buyer Mortgage Pre-approval, you’ll know exactly how much you can afford to spend on your first home. This empowers you to negotiate from a position of strength, knowing that financing will not be an issue when your offer is accepted.

Important Factors of the First Time Home Buyer Process

Pre-Approval vs. Full Approval

It’s common for first time home buyers to misconceive a pre-approval as a full-approval, or simply an approval, during the process of applying for a first time home buyer mortgage. A pre-approval is only preliminary estimates, not a guarantee. A pre-approval is a non-binding assertion that you are eligible for a loan up to a particular amount and is an estimate of your eligibility budget for both your home and mortgage. On the other hand, the approval is already the attainment of your specific loan of a specific amount.

Inspection and Appraisal

An inspection and appraisal are key components of the first home buying process which is especially important to look into for first time buyers. Before you move on to making a bid or securing a deposit, a further look into the house value is necessary. As the buyer, you are responsible for initiating the inspection process and therefore will have to carry the costs. This often intimidates first time home buyers as it adds yet another expense to the list. However, inspections are not very costly and are very well worth it in the long term if you can shave thousands of dollars off the price of the house. The condition and value of the property are not always up to par with the price a seller posts and there are likely to be hidden flaws that are not brought to your attention without an inspection. Once a licensed appraiser reviews and provides their unbiased report of the property value, you can renegotiate the prices with the seller.

Deposit

First time home buyers must be aware that they may very well need to pay a deposit alongside the initial purchase offer. A deposit intends to demonstrate to the seller that you are a serious buyer compared to others in the market who may be looking for a no deposit property. This money is put towards the overall price of the house and will be. There is no fixed amount that you are required to give as a deposit, but you’ll find buyers often provide up to 20% of the house price as a deposit. However, since you are a first time home buyer, keep in mind that there are instances when your deposit may be non-refundable even without the seller choosing you to purchase it. For this reason, it’s important to cooperate with your lawyer or your real estate agent about the possible consequences of the deposit before opting for it.

Down Payment

You just paid a deposit, now it’s necessary to pay a down payment? It’s a common misconception among first time home buyers that a deposit and down payment are referred to as the same thing. However, there is a sheer difference between the two. The deposit is often otherwise referred to as a security deposit and is an act of goodwill towards your seller. On the other hand, the down payment is related to your first time home buyer mortgage and you will still be required to pay the down payment for your mortgage even though you have paid a deposit. The amount you pay as a deposit is shaved off of the house’s total price, while the down payment goes towards your first time home buyer mortgage payments.

First-time homebuyers in Ontario can qualify for a rebate equal to the full amount of their land transfer taxup to a maximum of $4,000.

The Home Buyers’ Plan (HBP) is a program that allows you to withdraw up to $25,000 in a calendar year from your registered retirement savings plans (RRSPs) to buy or build a qualifying home for yourself or for a related person with a disability.

The FTHB Tax Credit offers a $5,000 non-refundable income tax credit amount on a qualifying home acquired after January 27, 2009. For an eligible individual, the credit will provide up to $750 in federal tax relief.

This benefit isn’t exclusive to first-time home buyers, but they can certainly benefit from it! There are a variety of rebates you can receive by making sure your home is energy efficient.

You may qualify for a rebate of part of the GST or HST that you paid on the purchase price or cost of building your new house, on the cost of substantially renovating or building a major addition onto your existing house, or on converting a non-residential property into a house.

We have you covered!

We have you covered!