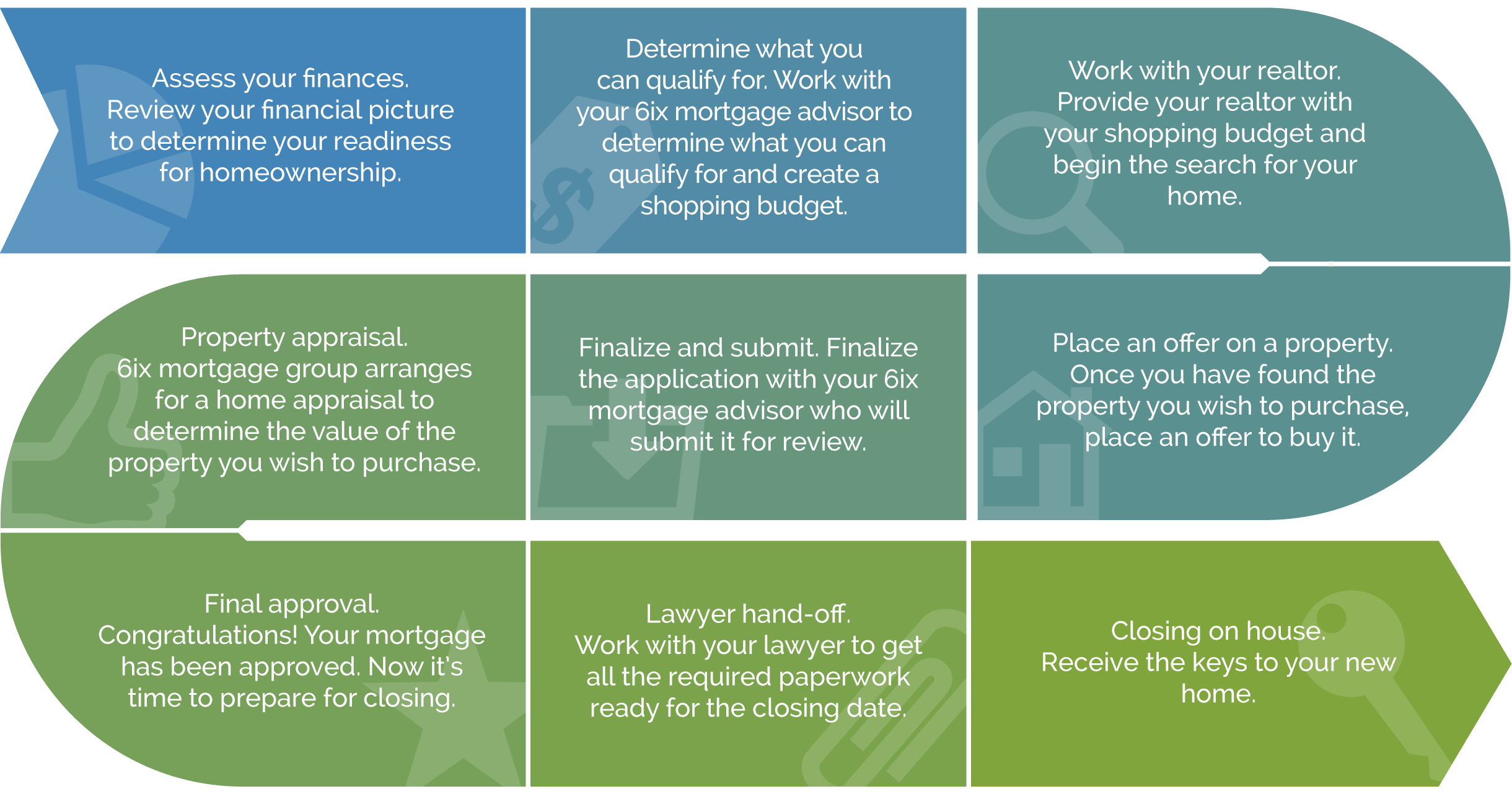

Construction mortgages are increasingly popular in Ontario with many choosing to build custom homes to meet their specific needs. Designing and building a custom home can be exciting, but it also comes with a unique set of financial challenges.

Qualifying for financing the construction of a new home is very different than qualifying for a mortgage to buy an existing home.

Financing is provided when a home is being built in stages and requires multiple advances of money over a period of time.

Here is what you need to consider:

Who will be building/renovating the property? Where applicable, the builder/contractor and the property must be registered under the applicable provincial New Home Warranty programs. If a builder/contractor (or you as the owner) is planning to construct the house, you will need to consider the builder/contractor’s ability to complete the project and any work you may intend to undertake on your own.

How long will it take to construct the property? The maximum construction period is one year from the date of the first advance.

What will construction cost? You need to have an idea of the total cost of construction. This estimate must include the land, building costs, site preparation including municipal services and finishing, and “soft costs” – non-building costs such as interest, required permits, real estate/solicitor fees, etc. In many cases, unexpected costs may arise, or you may wish to make changes, so you’ll need to make provision for those as well. It is recommended that you set aside an additional 15% of the estimated costs to cover unexpected overruns.

How much equity (down payment) do you have available? From what sources? The minimum down payment required depends on the appraised value or cost to construct (whichever is less) and the amount you want to borrow. The down payment must be available at the time of application.

When and how will the money be made available? Construction financing is advanced in parts (called “draws”) throughout construction via your solicitor. Each time a draw is requested, the construction work completed thus far must be inspected by an appraiser to confirm completion to that stage.

What documentation is required to apply?

Construction contract including costs

Construction plans or blueprint of the home.

If self-building, all quotes for labor and material.

Site preparations including municipal services for the lot.

For the land, a confirmation of ownership: if purchasing, a copy of the unconditional purchase and sale agreement.

Confirmation of required funds to bring construction to 35% completion stage.