If you’ve been wondering whether mortgage rates are about to move again, the latest take from TD Bank’s economics team gives a pretty clear hint:

If the Bank of Canada does anything next… it’s more likely a rate cut than a hike.

So… why are rate cuts even on the table?

According to Derek Burleton, Canada’s economy has taken hit after hit over the past few years:

- Pandemic chaos

- Inflation spikes

- Rapid rate hikes

- Trade tensions

- Middle East conflict pushing oil prices up

- AI starting to mess with the job market

And somehow, we’re still standing. Consumer spending is holding up well, and jobs haven’t collapsed. The economy isn’t booming, but it’s not breaking either. Economists are referring to this as ‘resiliance’.

Why that matters for rates

Here’s the key idea:

- The last time rates went up, it was because demand was too strong and inflation got out of control

- This time, inflation pressure is coming more from external shocks (like oil prices), not runaway spending

Because of this, instead of aggressively hiking again, the bar for raising rates is now very high, so unless something unexpected happens, the most likely scenarios are:

- Rates stay where they are

- They eventually come down

What could actually trigger a rate cut?

A few things could push the Bank to ease:

- Slower economic growth

- Weakening job market (especially if AI disruption ramps up)

- Consumers pulling back due to higher costs

- Housing staying soft longer than expected

On the flip side, the main thing that could delay cuts is oil. If the conflict in the Middle East keeps energy prices high for months, that could keep inflation sticky.

Quiet strength you might not be noticing

There are a few under-the-radar reasons Canada is holding up better than people expected:

1. The Canadian dollar is stable

Strong investment flows into Canada (especially pensions and resources) are helping support it.

2. The job market isn’t collapsing

Even though hiring isn’t booming, immigration slowing down has kept unemployment from spiking.

3. Oil is a double-edged sword

Higher gas prices hurt consumers in places like Ontario but boost provinces like Alberta and increase government revenue.

What’s happening with housing?

The reality is that in bigger provinces, such as Ontario:

- Prices are still soft

- Sales are slow

- Condo inventory is high (especially in the GTA)

Burleton’s take is that we’re likely:

- Near the bottom phase of this cycle

- Heading into stabilization over the next 1–2 years

- Then gradual recovery after that

Essentially a slow upward grind.

Also interesting:

The next wave of demand probably won’t be investors, it’ll be:

- First-time buyers

- Move-up buyers

- People who’ve been waiting on the sidelines

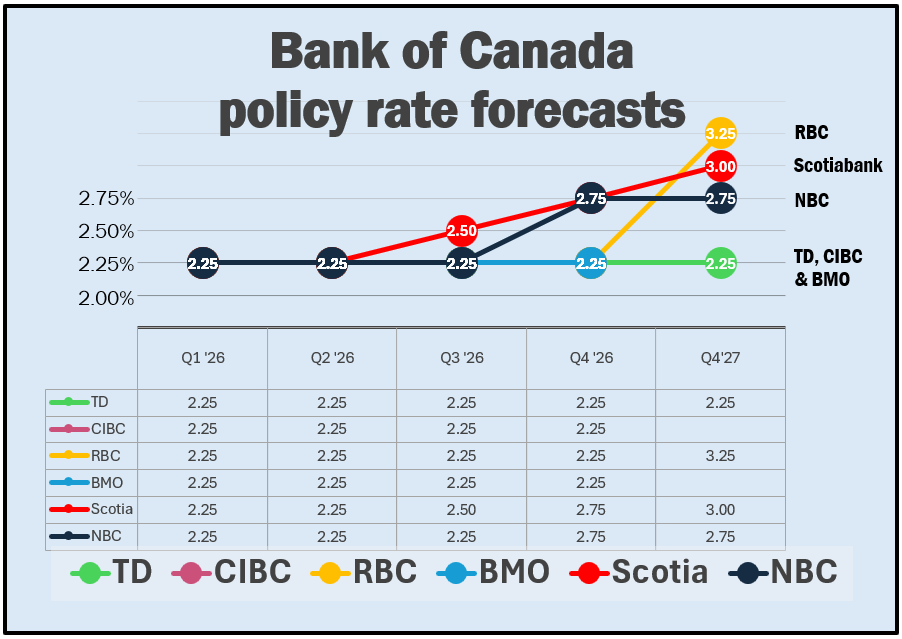

What Do The Other Banks Say?

According to TD, If you’re a homeowner or buyer:

- The rate hiking cycle is very likely done

- The next meaningful move is probably downward

- But timing is still uncertain

So right now we’re in this weird middle zone where:

- Fixed rates are already pricing in some future cuts

- Variable rates are waiting for the Bank to actually move

What other banks say, however, tell a different story:

Scotia, National Bank, and RBC all anticipate rate hikes by the beginning of 2027. This clearly shows a divide in the sentiment of which direction variable rates could end up. Keep in mind that these forecasts are always updating based on economic factors, so they could very well change as soon as next week.

My take as a mortgage broker

This is the kind of market where strategy matters more than ever.

Depending on your situation, you might be thinking about:

- Locking in a fixed rate now before cuts fully hit

- Staying variable to ride potential decreases

- Refinancing or restructuring ahead of changes

I personally feel that fixed rates have near bottomed-out, and have priced in any future rate cuts. Variable rates have a lot of potential, but we have no idea where rates will be 2-5 years from now, so it is not practical to predict what will put you ahead and whether variable will stay lower than fixed. Your best option here is to assess your risk tolerance, what helps you sleep at night, and what your long term plans are for your property.