If you’ve been watching mortgage rates lately, you may have noticed something interesting.

Just a couple weeks ago, 3-year fixed uninsured mortgage rates were around 3.69%.. Now we’re already seeing them closer to 3.89%

So what changed?

In short: the global markets. And right now, global markets are reacting to the war in Iran.

Let’s break down what’s happening in simple terms.

The Iran War Is Shaking Energy Markets

The conflict involving Iran has triggered a big shock in oil markets.

Oil prices have surged after fears that supplies could be disrupted, especially through the Strait of Hormuz, which handles about 20% of the world’s oil shipments.

At a point, oil prices spiked dramatically, jumping up toward $120 per barrel after rising as much as 28% in a single move as the conflict escalated.

When oil jumps like that, investors immediately start worrying about inflation coming back.

And that is where mortgages come in.

Why Oil Prices Affect Mortgage Rates

In short:

- War increases oil prices

- Higher oil prices increase inflation risk

- Investors sell government bonds

- Bond yields rise

- Fixed mortgage rates follow those bond yields higher

This is exactly what we’re seeing right now.

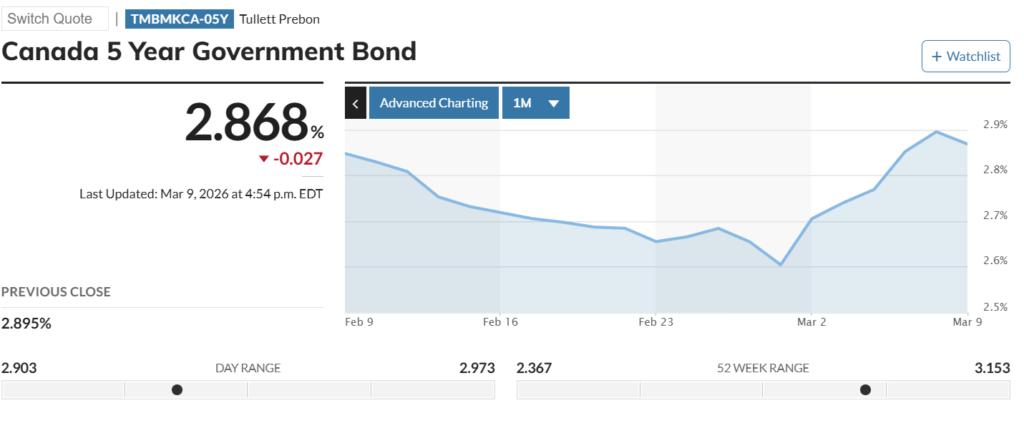

Canada’s 5-year government bond yield, which heavily influences fixed mortgage pricing, recently surged toward 2.868% as the Middle East conflict pushed oil prices higher and revived inflation fears.

When bond yields move up quickly, lenders reprice their fixed mortgages almost immediately.

Why Fixed Rates Move Faster Than Variable

This situation is a good reminder that fixed and variable mortgage rates behave very differently.

- Fixed rates follow bond markets and can change daily.

- Variable rates follow the Bank of Canada’s policy rate and only change when the central bank moves.

So even if the Bank of Canada hasn’t done anything, fixed rates can still rise or fall based on global events like wars, inflation scares, or financial market volatility. The Bank of Canada meets 8 times a year to decide on which direction to go with variable rates. The common question we still get is whether this effects variable rate discounts; the short answer is no. The discounts move independent to the bond yields increasing/decreasing.

Could Rates Go Higher?

The markets are currently trying to figure out two things:

- How long the conflict will last

- Whether oil prices will stay elevated

If oil remains high, inflation expectations could stay elevated too, which would likely keep bond yields and fixed mortgage rates higher.

But if tensions ease and oil prices fall back down, we could see mortgage rates stabilize again. For now, fixed rates are starting to increase across the board with several lenders.

Final Thoughts

Mortgage rates are influenced by a lot more than just Canadian housing data.

Global politics, oil markets, inflation expectations, and bond markets all play a role.

Right now, the war in Iran has created a shock that’s pushing oil prices higher and bond yields up and fixed mortgage rates are following along.

The big question now is whether this is a temporary spike or the start of a longer trend.

Either way, it’s a good reminder of how quickly mortgage markets can move.